Contactless payments have significantly improved how people around the world make purchases. According to a Mastercard report, contactless payments account for over 60% of all credit card transactions and 70% of all debit card transactions in the UK. Similarly, Visa reported that as of December 2022, 54% of face-to-face transactions in the U.S. were contactless.

In many countries, tapping a card or smartphone to a payment terminal takes just a few seconds, and you’re on your way. But if you’ve been following the Nigerian market, you might have noticed fewer real-life deployments compared to the many announcements. So, what’s really going on behind the scenes?

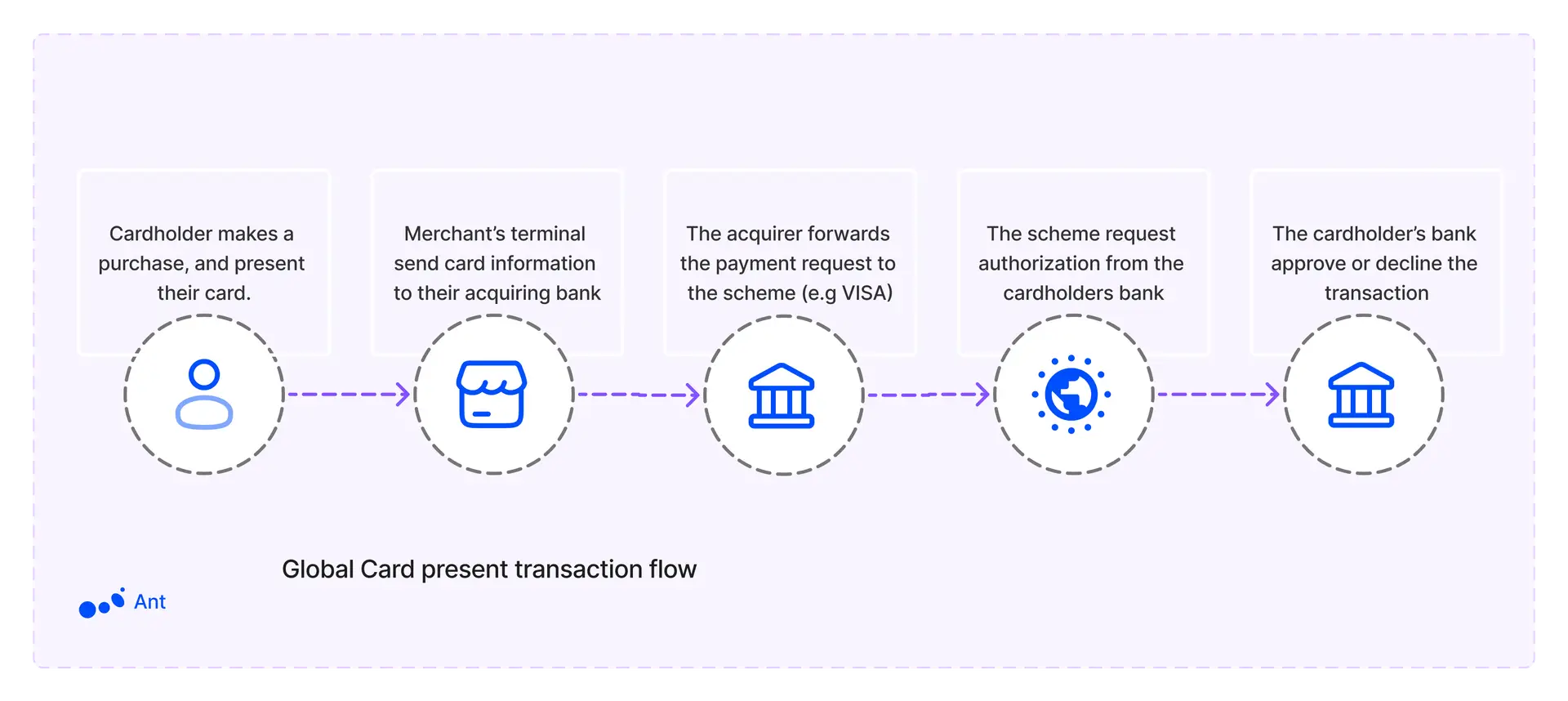

Lets Look at the Global Model

In most parts of the world, card-present transactions follow a fairly straightforward pattern:

Below is a simple illustration of this global card-present transaction flow:

- Cardholder makes a purchase and presents their card.

- The merchant’s terminal sends the transaction details to an acquiring bank.

- The acquirer forwards the request to the payment scheme (e.g., Visa or Mastercard).

- The scheme requests authorization from the cardholder’s issuing bank.

- The issuer approves or declines, and the response flows back through the chain—often in milliseconds.

It’s clean, direct, and relies heavily on established networks and protocols.

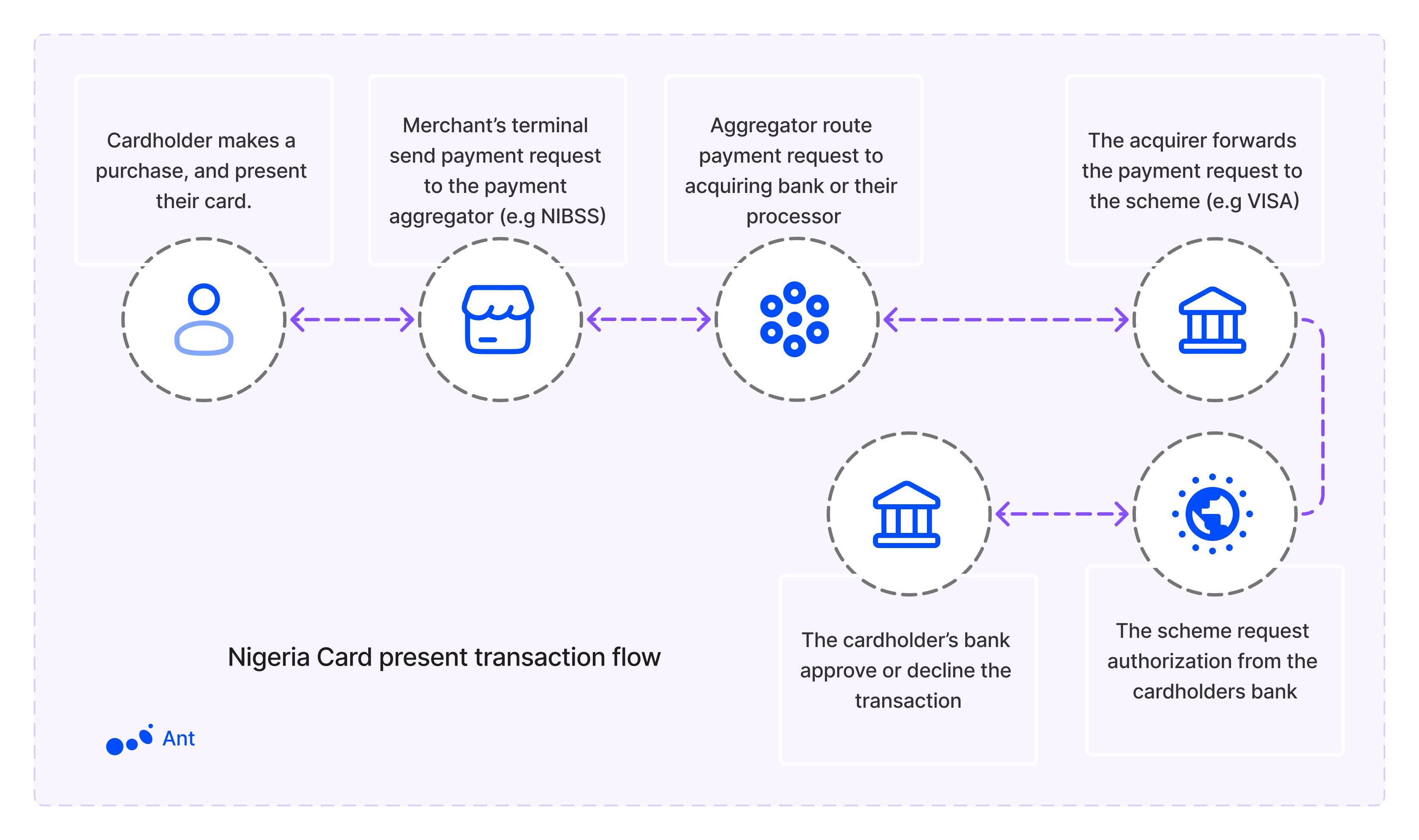

How Nigeria’s Model Differs

Nigeria’s payment landscape adds extra layers, partly because of regulatory requirements and a desire to keep transactions within local infrastructure. Instead of a merchant’s terminal directly communicating with an acquiring bank, the transaction often routes through a central aggregator—before reaching the acquiring bank or processor. From there, it eventually goes to the card scheme and the issuing bank.

Below is an example of the Nigeria card-present transaction flow:

This additional step ensures compliance with local guidelines and oversight from bodies like the Nigeria Inter-Bank Settlement System (NIBSS). While it enhances security and control, it also adds complexity. For a contactless solution—especially “Tap on COTS” (using standard mobile devices as payment terminals)—developers must navigate these extra regulations which was originally designed for traditional payment terminal, certifications, and integrations of the legacy portal. That’s one of the many reasons why many big announcements about “tap-to-pay” solutions can take a long time to translate into actual, widely available products.

Beyond the Technology: The Challenges

- Regulatory Approvals

- Each player—banks, fintechs, processors—must align with local rules.

- Extra certification steps prolong the launch timeline.

- Aggregator Integration

- Nigeria’s aggregator/TMS structure can require multiple rounds of testing.

- Any mismatch in data formats or security protocols can halt progress.

- Contactless payment was designed to be lightweight on device, but delegated most processing to the server for improved security. The design does not follow the legacy system design of traditional payment terminal introducing many technical bottlenecks that could take several months and even years to build around.

- Hardware and Software Requirements

- Even with software-based POS (Tap on COTS), you need to meet specific hardware security standards.

- Achieving the required “contactless readiness” isn’t as plug-and-play as it may seem elsewhere.

- Market Readiness

- While consumers appreciate speed, merchants must be convinced of the benefits.

- Educating end-users about tapping their card or phone is another step, especially in regions where cash is still king.

Ant’s Whitelabel Contactless Solution

Despite these hurdles, contactless payment is bullish in Nigeria—and it’s only a matter of time before it becomes more common. That’s where Ant steps in. We’ve built a compliant contactless payment system tailored for Nigeria’s unique environment. Instead of spending months wrestling with technical complexities, local aggregator requirements, and stringent regulations, banks and fintechs can adopt our whitelabel solution to:

- Launch faster: Integrate our solution and reduce development time.

- Stay compliant: We handle the local aggregator connections and regulatory details.

- Focus on your customers: Spend less time on backend engineering and more on building user-friendly experiences.

We don’t want to be “salesy,” but if you’re a stakeholder in the Nigerian payment space, you understand how crucial it is to get this right. Our goal is simple: help you roll out a secure, frictionless tap-to-pay experience that benefits everyone, from tech-savvy consumers to merchants in peri-urban areas.

Join the Conversation

If you’re curious about how we can help your bank or fintech bring contactless solutions to market without months of reinventing the wheel, reach out or drop a comment. Let’s collaborate to make Nigeria’s payment landscape as fast, safe, and convenient as it can be.

In the meantime, keep an eye out for those “tap-and-go” terminals—they might just be powered by Ant.